I see this question pop up constantly in financial reports and accounting discussions.

You know what capitalization means. You’ve seen assets added to the balance sheet. But when those assets come off the books? That’s where things get murky.

Discapitalied (or more commonly, decapitalization) is the reverse process of capitalization. It’s when you remove a previously capitalized asset from your books.

Most business owners focus on building their asset base. They miss how removing those assets can hit their financials harder than they expect.

I’ve reviewed hundreds of financial statements where this process confused investors and business owners alike. The terminology isn’t standard across all accounting practices, which makes it worse.

This guide walks you through what discapitalied actually means in accounting terms. I’ll show you the step-by-step process and explain exactly how it impacts your balance sheet, income statement, and cash flow.

No accounting degree required. Just straight talk about what happens when assets leave your books and why it matters for your financial picture.

Foundation First: What Does It Mean to Capitalize an Asset?

Let me ask you something.

When your business buys a $50,000 delivery truck, should that hit your books as a $50,000 expense today?

Most people new to accounting think yes. That’s what it cost, right?

Wrong.

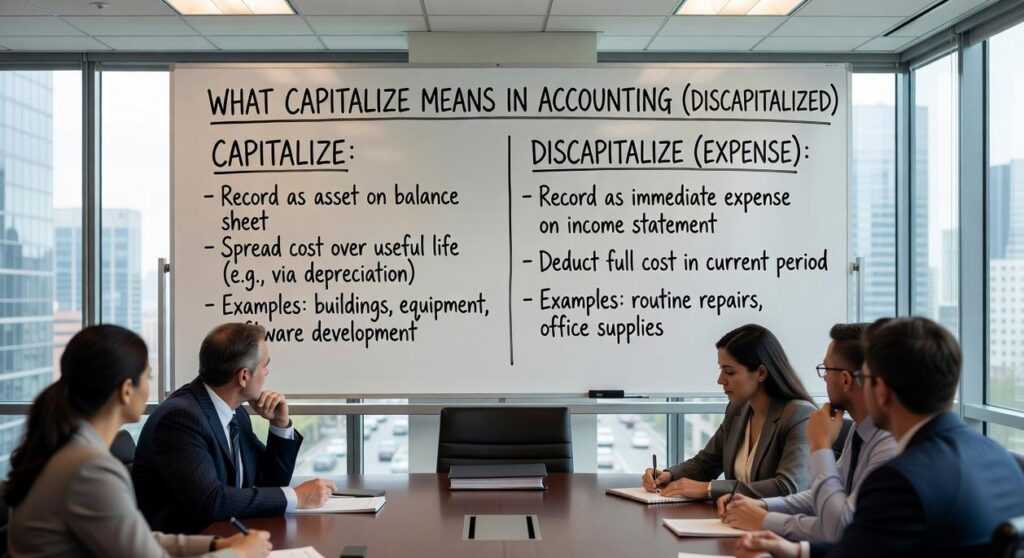

Here’s what capitalize means in accounting discapitalied. You record that cost as an asset on your balance sheet instead of an expense on your income statement.

Why does this matter?

Because that truck isn’t just benefiting you this month. It’ll help you make money for YEARS.

The rule is simple. If something gives you economic benefit beyond one accounting period, you capitalize it. If it gets used up this period, you expense it.

Think about it this way. Office supplies? Those get used up fast. Expense them. A delivery vehicle that’ll run for five years? That’s an asset.

Now some accountants will tell you this is just about following rules. That you should capitalize because GAAP says so.

But that misses the point.

Capitalizing gives you a clearer picture of what’s really happening in your business. When you expense that $50,000 truck all at once, your profit takes a massive hit. Your financials look terrible for no good reason.

Instead, you spread that cost over the truck’s useful life through depreciation. Maybe $10,000 a year for five years.

Your balance sheet shows the asset. Your income statement shows a reasonable annual cost. And your profitability looks WAY more accurate.

For small business owners who track asset purchases and disposals, tools like FreshBooks software can simplify how capitalization and discapitalization are recorded in real time.

That’s the real benefit here.

The Core Concept: What Does ‘Discapitalied’ Mean?

Let me break this down in plain terms.

Discapitalied means you’re taking an asset off your company’s books. It’s not an official accounting term you’ll find in GAAP or IFRS manuals, but people in business use it all the time when they’re talking about getting rid of assets.

Think of it this way. When you first buy equipment or property, you capitalize it. That means it goes on your balance sheet as an asset. But eventually, that asset needs to come off.

Here’s when that happens.

You sell the asset to someone else. Maybe you upgraded your machinery and sold the old stuff. Or you scrapped it because it stopped working and repair costs don’t make sense anymore. Sometimes the asset gets fully depreciated and you take it out of service (it’s done its job). Other times you lose it to damage or theft. And occasionally, you realize it’s just worthless and write it down through impairment. In the world of gaming asset management, it’s crucial to recognize when an item has been fully utilized and is effectively “Discapitalied,” prompting players to make strategic decisions about whether to sell, upgrade, or scrap it altogether.

The goal is simple. You want your balance sheet to show only what you actually own and use right now. Not what you owned three years ago.

So when you discapitalize an asset, you remove both its original cost and all the accumulated depreciation tied to it. This keeps your financial records clean and accurate.

Here’s a real example. Say you bought a delivery van for $30,000 five years ago. You’ve been depreciating it, and now it’s worth $5,000 on your books. You sell it for $6,000. You need to remove that van from your records entirely and account for the $1,000 gain.

That’s what what capital can you allocate Discapitalied is all about. Keeping your books honest.

The Step-by-Step Process of Discapitalizing an Asset

Most people think removing an asset from your books is simple.

You just delete it and move on, right?

Wrong.

I see this confusion all the time. Business owners treat discapitalizing like it’s some quick accounting trick. They assume it’s the same whether you’re selling equipment for a profit or junking a broken machine.

But here’s what actually happens.

The process changes based on your situation. Selling an asset for more than its book value looks completely different from scrapping something worth zero.

Let me walk you through this.

Step 1: Identify the Asset and Triggering Event

First, you need to know exactly what you’re removing and why. Are you selling it? Scrapping it? Donating it?

This matters because each scenario affects how you record the transaction.

Step 2: Calculate the Asset’s Book Value

Take the original cost and subtract all the depreciation you’ve recorded over the years. That’s your book value.

Book Value = Original Cost minus Accumulated Depreciation. For the full picture, I lay it all out in Discapitalied Economy Updates From Disquantified.

Simple math, but you need accurate records.

Step 3: Determine the Gain or Loss

Now compare what you’re getting (if anything) to that book value.

Scenario A: Selling Above Book Value

Say you bought equipment for $10,000. You’ve depreciated $6,000 of it. Your book value is $4,000.

You sell it for $5,500. That’s a $1,500 gain.

Scenario B: Selling Below Book Value

Same equipment, same $4,000 book value. But you only get $2,800 for it. In light of the recent Finance Updates Discapitalied, it’s disheartening to see that despite having the same equipment valued at $4,000, you can only expect to receive a mere $2,800 for it.

That’s a $1,200 loss.

Scenario C: Scrapping with Zero Proceeds

You can’t sell it at all. It goes to the dump.

Your loss equals the entire remaining book value of $4,000.

Step 4: Record the Journal Entry

This is where you actually remove the asset from your books. You’ll debit accumulated depreciation, credit the asset account, record any cash received, and recognize your gain or loss.

(Your accountant will handle the specifics, but you should understand what’s happening.)

The key difference between these scenarios? How they hit your income statement. A gain boosts your profit. A loss reduces it. And scrapping an asset with remaining value? That can hurt.

The Significance: How Discapitalization Impacts Financial Statements

Here’s what most accounting textbooks won’t tell you.

When a company removes an asset from its books (what capitalize means in accounting discapitalied), it’s not just some boring bookkeeping exercise. It tells you a story about what’s really happening inside that business.

And honestly? I think investors miss this signal way too often.

Let me break down what actually happens when a company discapitalizes an asset.

The balance sheet takes the first hit.

The Property, Plant, and Equipment line drops by whatever the asset originally cost. Accumulated Depreciation (that’s the running total of wear and tear) also drops by the same amount. If they sold the asset, cash goes up. Pretty straightforward.

But here’s where it gets interesting.

The income statement shows you the real story.

You’ll see either a Gain on Sale or a Loss on Disposal pop up. Usually in that Other Income section where companies bury stuff they don’t want you focusing on (I always look there first, by the way).

The thing is, once that asset is gone, so is the depreciation expense. That means net income goes up in future periods. Some analysts love this. I think it can hide problems if you’re not paying attention.

The cash flow statement completes the picture.

Any cash from selling the asset shows up in Investing Activities. Meanwhile, that gain or loss gets backed out of Operating Activities because it’s not actually cash.

Now here’s my take on why this matters.

When I see a company dumping assets left and right, I get curious. Maybe they’re upgrading their tech. Maybe they’re pivoting strategy. Or maybe (and this is what worries me) they’re scrambling for cash.

You need to look at the volume and pattern. One or two disposals? Normal business. A flood of them? That’s a red flag worth investigating through finance updates discapitalied.

I also watch what it does to performance ratios. Return on Assets can suddenly look better just because the denominator got smaller. Fixed Asset Turnover might spike. But are those improvements real or just accounting artifacts?

Most investors I talk to ignore this stuff. They focus on revenue and earnings and call it a day.

That’s a mistake.

The way a company manages its asset base tells you how management thinks. Are they investing in growth or milking what they have? Are they being strategic or desperate?

Look, I’m not saying every asset disposal is bad. Sometimes it’s exactly the right move. But you need to understand what’s happening on these three statements to know the difference. When evaluating whether a game studio has effectively capitalized on its assets or has become Discapitalied, it’s crucial to analyze the implications of their financial statements to make informed decisions about their future.

Understanding the Full Asset Lifecycle

You now know what discapitalizing means in accounting.

It’s the final step in an asset’s life. You remove it from the balance sheet when you sell it or dispose of it.

A lot of people think this is just paperwork. It’s not.

Discapitalizing creates real entries across all three major financial statements. The asset comes off your books. You record a gain or loss on your income statement. Cash flow changes depending on how you disposed of it.

This matters because it tells you what a company is actually doing. Are they selling off assets to raise cash? Did they get a good price or take a loss? These decisions reveal operational health and strategy.

Here’s what you should do: Next time you analyze a financial report, look at the investing activities section in the cash flow statement. Check for any gains or losses on asset sales in the income statement.

Those line items tell the real story behind the numbers.

When you understand discapitalizing, you see the complete picture of how assets move through a business. That’s how you make better investment decisions.

Xyphina Tornhanna has opinions about investment strategies and tips. Informed ones, backed by real experience — but opinions nonetheless, and they doesn't try to disguise them as neutral observation. They thinks a lot of what gets written about Investment Strategies and Tips, Market Analysis and Trends, Expert Financial Advice is either too cautious to be useful or too confident to be credible, and they's work tends to sit deliberately in the space between those two failure modes.

Reading Xyphina's pieces, you get the sense of someone who has thought about this stuff seriously and arrived at actual conclusions — not just collected a range of perspectives and declined to pick one. That can be uncomfortable when they lands on something you disagree with. It's also why the writing is worth engaging with. Xyphina isn't interested in telling people what they want to hear. They is interested in telling them what they actually thinks, with enough reasoning behind it that you can push back if you want to. That kind of intellectual honesty is rarer than it should be.

What Xyphina is best at is the moment when a familiar topic reveals something unexpected — when the conventional wisdom turns out to be slightly off, or when a small shift in framing changes everything. They finds those moments consistently, which is why they's work tends to generate real discussion rather than just passive agreement.

Xyphina Tornhanna has opinions about investment strategies and tips. Informed ones, backed by real experience — but opinions nonetheless, and they doesn't try to disguise them as neutral observation. They thinks a lot of what gets written about Investment Strategies and Tips, Market Analysis and Trends, Expert Financial Advice is either too cautious to be useful or too confident to be credible, and they's work tends to sit deliberately in the space between those two failure modes.

Reading Xyphina's pieces, you get the sense of someone who has thought about this stuff seriously and arrived at actual conclusions — not just collected a range of perspectives and declined to pick one. That can be uncomfortable when they lands on something you disagree with. It's also why the writing is worth engaging with. Xyphina isn't interested in telling people what they want to hear. They is interested in telling them what they actually thinks, with enough reasoning behind it that you can push back if you want to. That kind of intellectual honesty is rarer than it should be.

What Xyphina is best at is the moment when a familiar topic reveals something unexpected — when the conventional wisdom turns out to be slightly off, or when a small shift in framing changes everything. They finds those moments consistently, which is why they's work tends to generate real discussion rather than just passive agreement.